These last few years I have been studying two issues: the integration of renewable energy into the grid, and the reform of electricity markets. By combining these I have been able to look at the design and reform of electricity markets in response to renewables integration. Market reform and renewables development is a two-way process. Electricity market rules, mechanisms and technology constrain the development of renewables, affect integration in the short term, and affect investment in the longer term. Meanwhile, greater market penetration by renewables means new challenges for traditional electricity markets in terms of security of supply and price fluctuations.

China's carbon neutrality and energy transition strategies mean the country is bound to develop renewables. The question is, how to achieve that at the smallest possible cost. Integration is key.

The challenges of integrating renewables

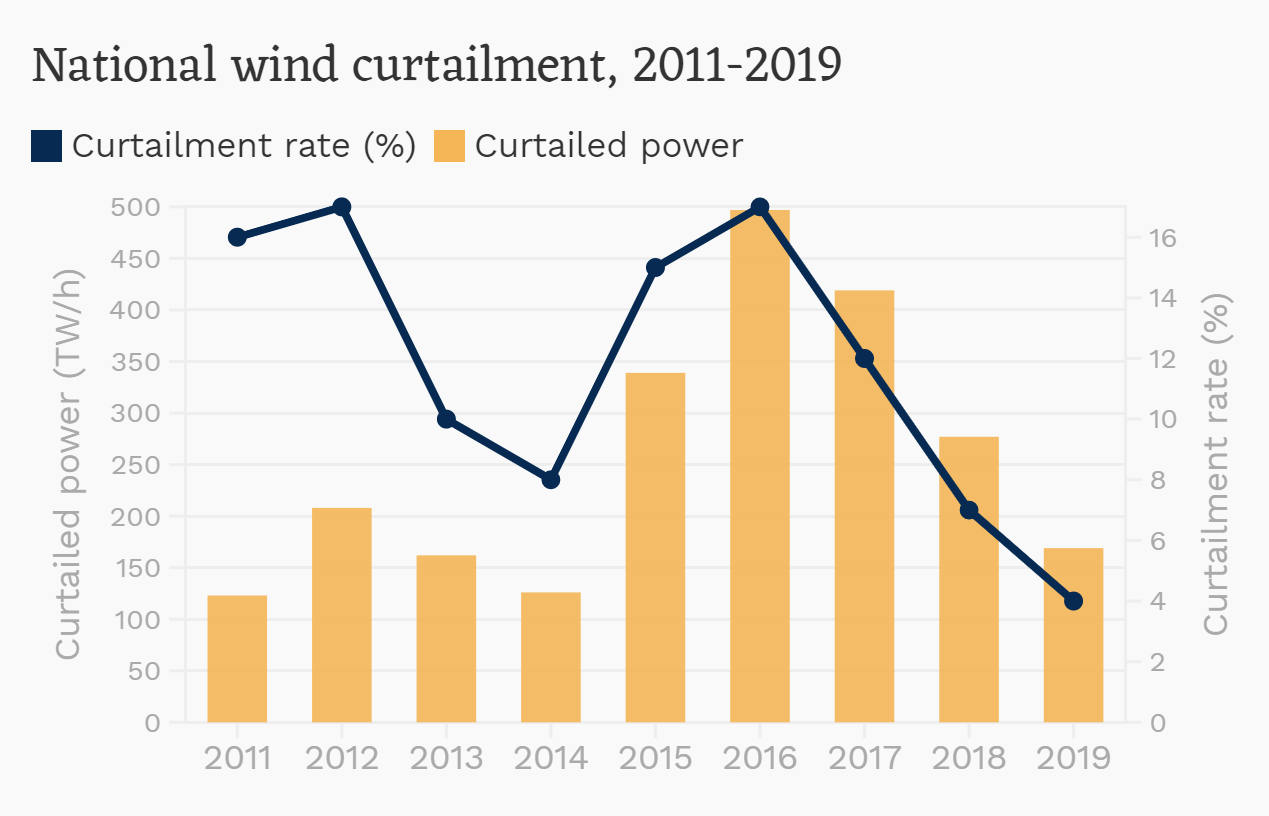

Renewables have developed rapidly in China. By 2014, it had the greatest wind power generating capacity of any country. But this process has been made more complex by “curtailment” – surplus energy produced but not consumed – of wind and solar power. As the chart below shows, the curtailment rates for wind power fell to 4% in 2019, and they should have dropped further to 3% in 2020. But the problem will reappear as capacity expands and the proportion of renewables in the energy mix increases. These challenges arise from three characteristics of renewable energy.

First, renewable energy levels can vary. Take the province of Qinghai: on a sunny day it generates huge amounts of solar power, particularly in the middle of the day. But in the evening, nothing. Wind power, meanwhile, picks up a bit overnight, but the output of both forms of power does not line up in time with actual demand.

Second, output fluctuates unpredictably with the weather.

Third, in China as in many other countries sources of renewable power are distant from areas of high demand, making large-scale integration of renewables a challenge.

The variability and fluctuation of renewable power sources present issues for the safe and reliable provision of electricity. Renewable power generation tends to be concentrated at particular times, in particular places, while mechanisms for electricity market clearing (the point where electricity supply equals demand) operate with low time granularity. For example, solar-generated power may only be bought a day ahead rather than in half-hour increments. This is unsuitable for the highly changeable costs of renewables’ generation and risks congesting the grid and unbalancing the market. While fuel costs for renewables are effectively zero, their presence on the market pulls prices downwards, reducing profits for fossil fuel-powered generation and making investment less likely. If this goes on, it could threaten adequate electricity supplies as traditional power generators remain essential for grid stability and responsiveness before electricity storage becomes an economic option.

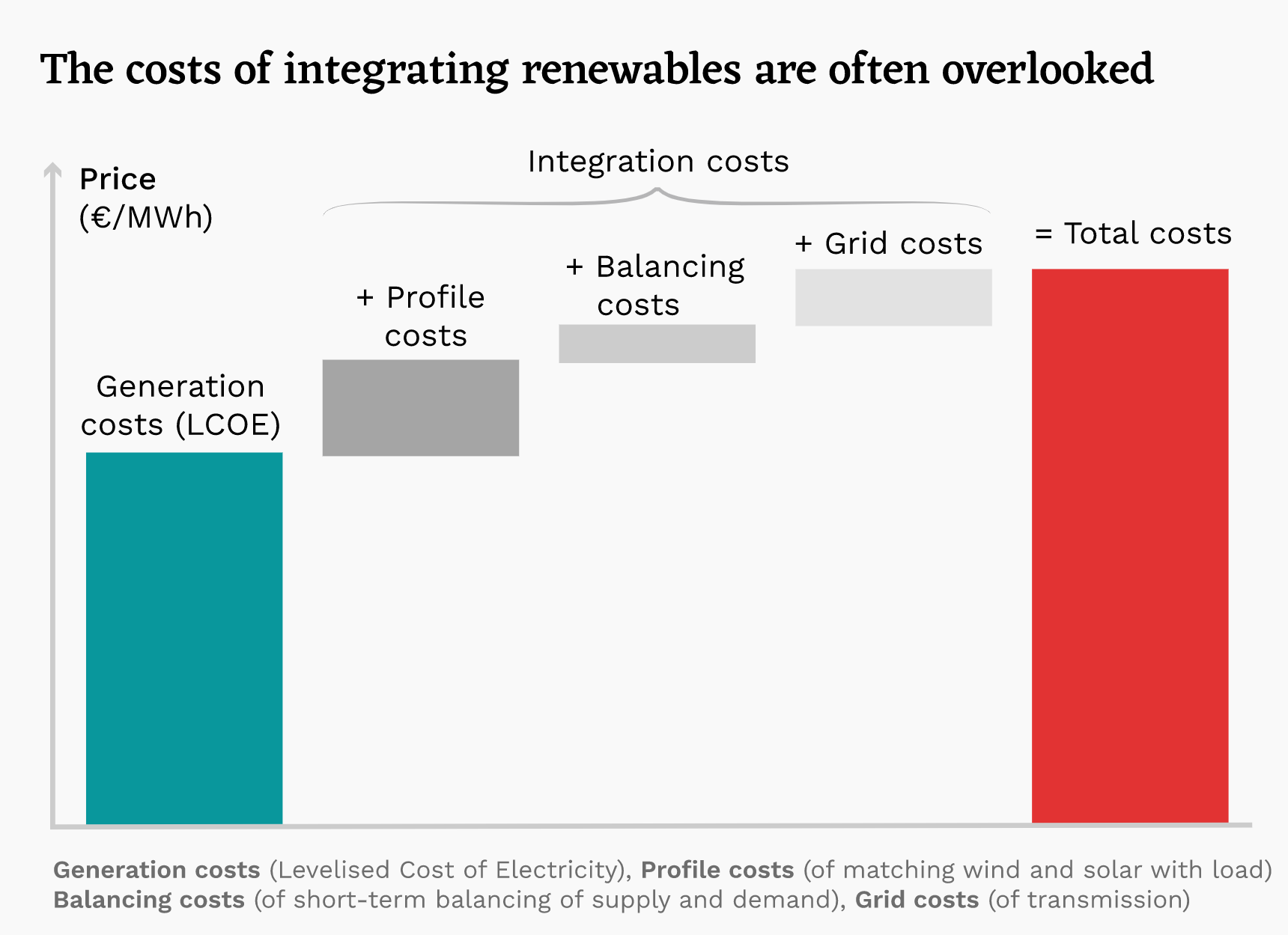

Another challenge is the “renewables paradox”. Although wholesale prices for renewable power are falling, retail prices are going up. Focus is currently on generation costs and achieving grid parity – where producing renewable energy costs the same as producing fossil fuel energy. On the generation side, renewables are competitive but, as we will see, generation is not the only cost. Thus our focus should shift to integration costs across the power system as a whole.

In Germany, wholesale prices for renewable energy started falling in 2012 but retail prices have risen steadily. According to a German government report, surcharges for renewable energy have consistently risen.

Those costs are closely related to the three characteristics of renewable energy discussed earlier. Variability of output increases the cost of matching generation with end users, while short-term fluctuation and uncertain output creates load-balancing costs. Changes in the location of generation requires investment in power grids, adding to the total cost of integrating renewable energy.

Chart 2 shows that traditional energy systems also have backup capacity costs, which increase as more renewables come online. Also, overproduction can cause costs to rise.

*Levelised Cost of Electricity (LCOE) is the full life-cycle costs of a technology per unit of electricity it generates • Source: Ueckerdt, F., Hirth, L., Luderer, G.,& Edenhofer, O. (2013). System LCOE: what are the costs of variable renewables?. Energy, 63, 61-75.

According to a 2020 review by Heptonstall and Gross of more than 40 papers studying the estimated costs of integrating renewables, those costs increase as market penetration increases, to a median of about 0.2 yuan per kilowatt hour when penetration is 20%.

Similar trends can be seen in China’s electricity markets. Some provinces already operate markets for power market ancillary services, particularly those that generate a lot of renewable energy. Costs for ancillary services are highest in the north-west and in provinces such as Xinjiang and Shaanxi, where this can reach over 3% of total on-grid power costs. One of the biggest problems integrating renewables poses for the electricity market is the phenomenon of “missing money”, which corresponds to the long-term adequacy of supply issue.

Some characteristics of generation capacity, such as “ramping capability” – the ability to respond to increased demand – were unimportant before market competition started and renewables came online. Now, responding to increasing demand quickly, or even instantaneously, is important. But the existing electricity market places no value on this, and so little attention is paid to providing it. With more renewables penetration, ramping capability is important and scarce, and the market should be designed to promote it. Otherwise, generation capacity will fail to make use of such advantages and in the long term there will be a lack of investment, reducing adequate supply to the electricity market.

To meet those challenges, the demand and supply curves need to be able to adjust in real time. How to encourage that? The market approach is to design mechanisms which issue finer-grained pricing signals across space and time.

Electricity markets 2.0

These challenges are forcing electricity markets to evolve.

A look at how electricity markets in Europe and the US have changed to accommodate renewables shows the key is more accurate reflection of supply and demand changes in market clearing prices. This makes granularity across time and location ever more important. For example, to ensure flexibility, time granularity of products on the market needs to run from several minutes to several years. Capacity market mechanisms ensure long-term supply. Nodal pricing, which prices electricity at given transmission nodes, better directs investment to certain locations. Electricity system operators start to appear, combining the real-time electricity market and ancillary services.

We can identify some principles arising during this process of evolution.

1. The ideal market will be able to set prices for scarce resources, taking into account all costs and benefits. Price signals will be reasonable and will guide production, consumption and investment. The market will reward flexibility and provide incentives to ensure long-term supply.

2. Government policy and market incentives should be compatible. For example, the electricity market should be in line with climate change policy.

3. Who benefits/pays? The market is a way to allocate resources, but also to allocate benefits, so if a power grid enjoys the services of a storage facility, it should pay for it.

4. The market should be flexible enough to accommodate new technology.

With these principles in place, the market will provide electricity at the lowest cost and greatest benefit.

But besides general principles of market design, we should face up to particular constraints China faces.

First, the issue of geography. China's generation of renewables is generally in the west of the country, while electricity demand is in the east.

Second, technological constraints. Flexibility, for example, is a challenge for technology as well as for the market. China still relies largely on coal-fired power, often from large plants, which are less responsive than gas-fired equivalents.

Third, constraints in the system, caused by the way the market works. The market is only in its first phase. Meanwhile, provincial trials of electricity market reforms have made variable progress as expected. Currently, everyone is focused on keeping electricity prices down, but our analysis has found lower electricity prices come mainly from removing surcharges and reducing transmission prices. And as the market is still being built, it naturally has some weaknesses: market and planned economy mechanisms exist side by side, the design of the market needs improvement, price signals are distorted and market supervision is inadequate.

If reforms focus on minimising prices, we'll see a rise in the use of small-scale coal-fired power, running contrary to climate policy.

So how do we get to the next stage?

First, we need smarter policies on renewables and new technologies. We should learn from past industrial policies, which sometimes achieved good results as an industry formed, but also had negative outcomes. For example, through distorting how power generators chose locations – for example, by subsidising renewable energy in Western provinces – and so increasing power costs. Future industrial and technology policies should be market-compatible.

Second, we need better market design that sends the correct price signals. Price fluctuations are to be expected because of market forces. We should avoid government price controls, and treat prices as a way to reallocate and rebalance assets. Also, we need to look at anti-monopoly measures, even planned pricing would be preferable to monopoly and cartel pricing.

Third, the market requires systematic high-level design. The electricity market is by nature complex, and renewables increase that complexity. If we want to build bigger electricity markets, the existing provincial electricity markets need to converge. That requires decisions to be made on complexity and practicality when designing markets.

Fourth, reforms of the electricity system and policies on climate change could be better coordinated. Our team's studies in southern China have found that if reforms focus on minimising prices we will see a rise in the use of small-scale coal-fired power, running contrary to climate change policy.

The key issue in developing renewables is integration. The cost of integration isn't just the cost of generation. In the future, overall integration costs need to be taken into account. If the market is to encourage the development of renewables, we will need innovation in market design, and if we want to use the market to solve problems and innovate, we need to be able to price more accurately, based on timings of supply and location. Building China's electricity market will be a long-term project, and moving to the next phase with require high-level design and steady progress.

相关新闻

-

应用经济学院党委举行庆祝中国共产党成立105周年表彰大会

2026/07/10

-

应用经济学院党委书记关晓斌讲授树立和践行正确政绩观学习教育专题党课

2026/07/10

-

应用经济学院、和平与发展学院2026年毕业欢乐颂系列活动举办

2026/07/05

-

应用经济学院党委在中国人民大学庆祝中国共产党成立105周年表彰中荣获佳绩!

2026/07/03